We love talking to you, our valued agents, but we know sometimes you just need a change made to a policy as quickly as possible.

So we’ve made it so you can do the most common changes whenever you need.

For example, on a Dwelling policy you can do a Non-Money endorsement or an Agent Money Endorsement by selecting Actions/Modify Policy. On the bottom of the Policy detail page you will see two buttons:

![]()

The Non-Money endorsement lets you change the Bill To, Pay By, Insured Name and information, Mailing Address and Additional Interest/Mortgagee information.

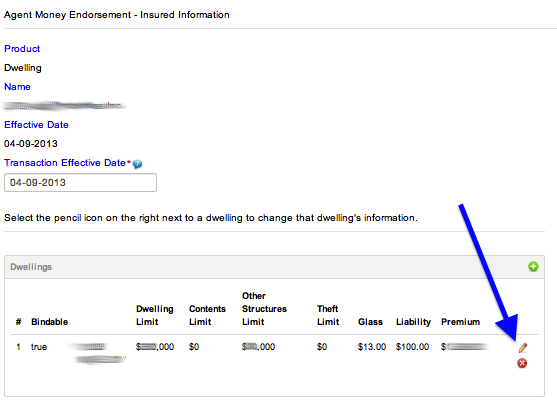

The Agent Money endorsement lets you change the age of the roof, the Other Structures limit and the Dwelling Update information. Simply select the dwelling you want to modify:

Then add or correct the information:

You can change all the same information on a Homeowners and MobileHome policy also.

On Renters policies you can add or delete Additional Insureds or make changes to Additional Insured name and address.

This is just another small part of how we work hard to make things as easy as possible for our agents.